From our point of view, market volatility initially spiked as investors need to adapt to a new interest-rate regime and the potential negative consequences on long-term economic growth. While we believe the uncertainty around the interest-rate and economic outlook should persist in the coming months, we also would like to highlight the importance of avoiding the natural tendency to overreact to short-term market volatility.

Successful investing needs thoughtfulness and composure, and we continue to rely on our macro, fundamental and market indicators instead of reacting ex-post to market action. Despite a potentially less supportive liquidity outlook in the months ahead, the weight of evidence leads us to maintain a positive stance on risk assets and equity in particular. Global growth remains above potential, financial conditions remain supportive, global earnings growth remains well oriented and some segments of the market remain reasonably valued. Our market technical indicators (trend, sentiment, etc.) continue to react rather nervously to recent market volatility but are not flashing red yet.

Key takeaways:

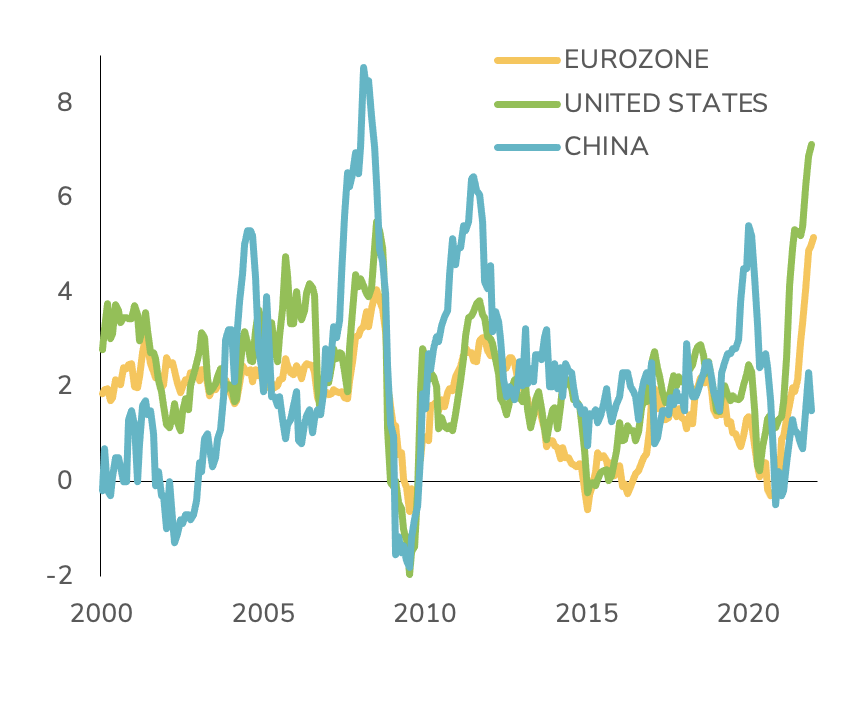

- From a macro perspective, we continue to believe that normalization in growth and inflation rates remains the central scenario for 2022. However, downside risks on growth and upside risks on inflation are increasing;

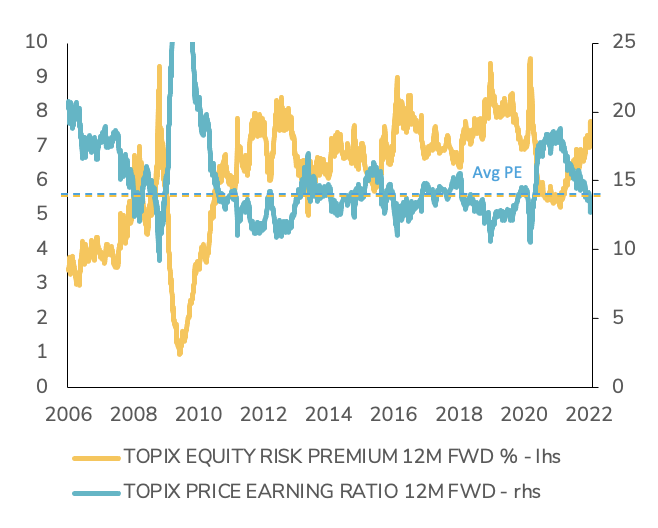

- We maintain a positive view on equities. The January pullback has reset investor expectations to more reasonable valuations. The most speculative fringe of the market is starting to look less pricey. Meanwhile, value and cyclical sectors continue to benefit from rising interest rates (Financials) and higher commodity prices (e.g Energy stocks);

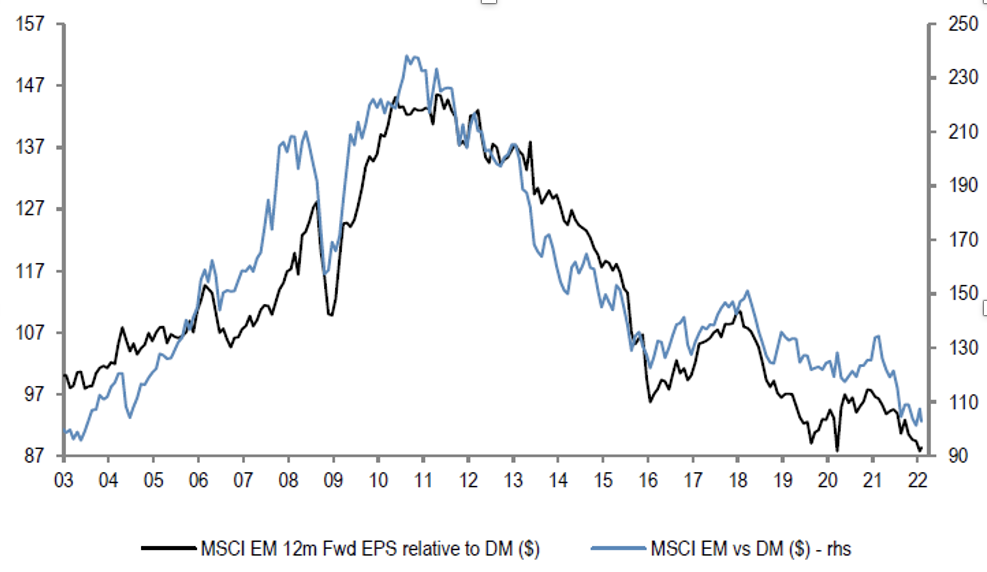

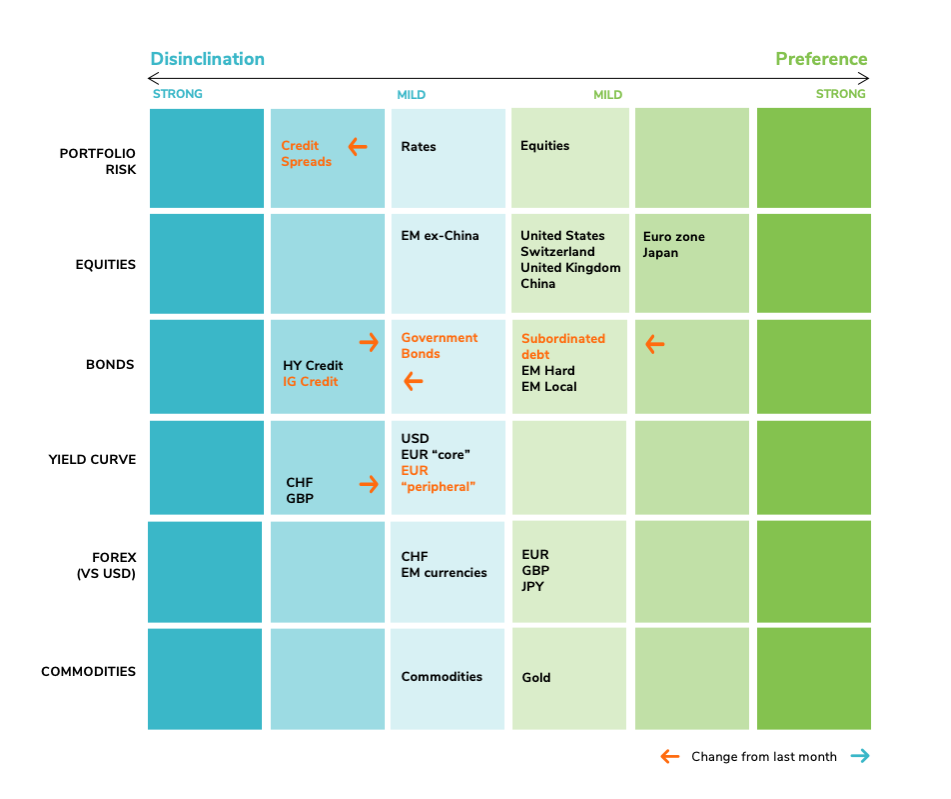

- Our preference remains for Eurozone and Japan equities, as both regionshave a positive bias towards cyclical and value sectors. We also remain positive on US, UK, Swiss and Chinese equities but keep a cautious stance on Emerging ex-China stocks;

- While we believe that equity markets could stabilize in the short-run, high yield and lower quality investment grade should continue to suffer from declining liquidity, rising interest rates (investors will be less likely to seek lower ratings for high yields) and tight valuations. We are thus downgrading credit spreads from “cautious” to “disinclination”. We remain cautious on rates;

- Within bonds, we are upgrading government bonds from “disinclination” to “cautious”, as we believe that the recent spike in benchmark bond yields has been quite brutal. We are downgrading Investment Grade Credit one notch to “disinclination”. From a yield curve perspective, we are cautious on USD, EUR “core” and EUR “peripheral”. Regarding the latter, our “disinclination” call last month proved to be correct and we are now upgrading EUR “peripheral” by one notch as we believe recent spreads widening already prices the hawkishness of the ECB;

- In Forex, we remain positive EUR, GBP and JPY against USD while still cautious on the Swiss Franc and EM currencies. We stay cautious on Commodities and positive on Gold.